| TAX REFORM 2018 |

| -Changes to 2018 tax preparation with implementation of the Tax Cuts and Jobs Act (TCJA)- |

| About the TCJA |

| "The Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018, Pub. L. 115-97, is a congressional revenue act originally introduced in Congress as the Tax Cuts and Jobs Act (TCJA), that amended the Internal Revenue Code of 1986." |

| Most sweeping tax reform in over 30 years that affects both individuals and businesses; estimated revision/creation of more than 400 taxpayer forms & instructions (more than double the amount in a typical year). |

| TCJA was signed into law by President Donald J. Trump on December 22, 2017. |

| Most changes did not apply until January 1, 2018 and remain in effect until December 31, 2025, pending further legislation. |

| Top |

| Tax Rate Changes |

| Individual Rates are lowered to 10%, 12%, 22%, 24%, 32%, 35% and 37% |

| Top |

| Standard Deduction Amounts Increased |

| Single $12,000 ... (up from $6,350 in 2017) |

| Married Filing Joint/Qualifying Widow(er) $24,000 ... (up from $12,700 in 2017) |

| Married Filing Separately $12,000 ... (up from $6,350 in 2017) |

| Head of Household $18,000 ... (up from $9,350 in 2017) |

| Top |

| Schedule A Itemized Deduction Changes |

Limit on overall itemized deductions for high-income AGI has been suspended Limit on overall itemized deductions for high-income AGI has been suspended |

| Deduction for state & local income, sales & property taxes is limited to $10,000 (see below) |

|

Home Mortgage/HELOC Interest

|

New Dollar Limit on Total Qualified Residence Loan Balance

|

| **Mortgage Interest Example: In January 2018, a taxpayer takes out a $500,000 mortgage to purchase a main home with a fair market value of $800,000. In February 2018, the taxpayer takes out a $250,000 home equity loan to put an addition on the main home. Both loans are secured by the main home and the total does not exceed the cost of the home. Because the total amount of both loans does not exceed $750,000, all of the interest paid on the loans is deductible. However, if the taxpayer used the home equity loan proceeds for personal expenses, such as paying off student loans and credit cards, then the interest on the home equity loan would not be deductible. |

Charitable Contributions

|

Casualty & Theft Losses

|

Miscellaneous Deductions

|

| Top |

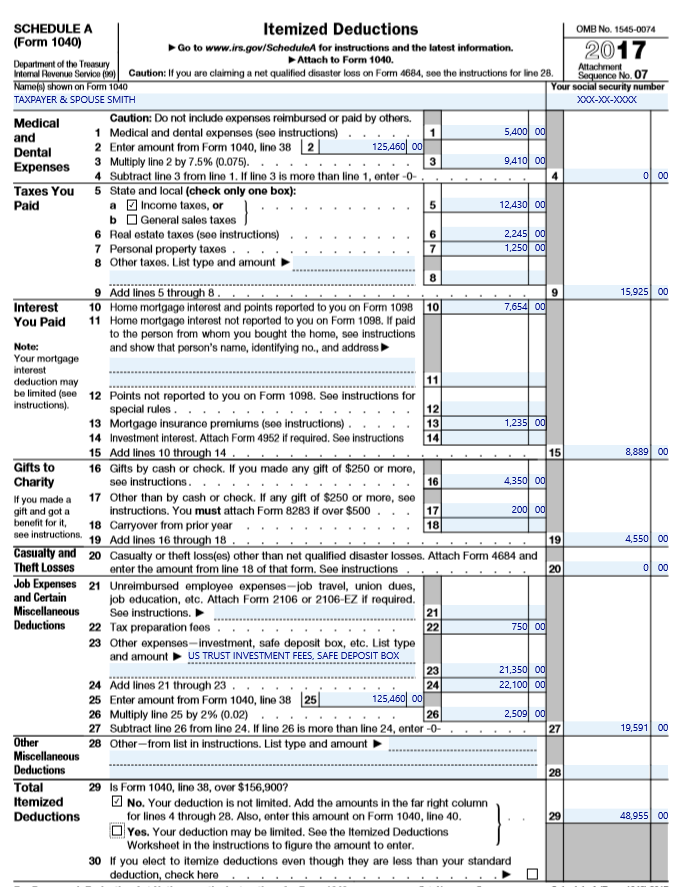

| Schedule A Example - Comparison from 2017 to 2018 |

| 2017 Schedule A - Taxpayer & Spouse (MFJ) were able to itemize their deductions of $48,955 which was higher than the standard deduction of $12,700 for the 2017 tax year. |

|

| 2018 Schedule A - Assume that for tax year 2018, Taxpayer & Spouse have relatively the same deductions. However, the taxes paid are limited to $10,000, mortgage insurance premiums aren't deductible and the Job Expenses & Certain Miscellaneous Deductions has been eliminated completely from Schedule A. These changes result in a standard deduction of $24,000 for the taxpayers. This is a decrease of $24,955 in deductions for the taxpayers. This could dramatically affect their tax bill for 2018 and reinforce why tax planning is important. |

|

| Top |

| Deduction & Exclusion for Moving Expenses |

| The deduction for moving expenses is suspended. No deduction is allowed for use of an automobile as part of a move. |

| The suspension does NOT apply to members of the U.S. Armed Forces on active duty who move pursuant to a military order related to a permanent change of station. |

| Employers will include moving expense reimbursement as taxable income in employees' wages. |

| Top |

| Personal Exemptions |

| For 2018, the deduction for personal exemptions has been suspended. You cannot claim an exemption for you, your spouse, or your dependents. |

| Top |

| Child Tax Credit (CTC) & Additional Child Tax Credit |

| The maximum credit increased to $2,000 per qualifying child ..... (up from $1,000 in 2017) |

| $1,400 of the credit can be refundable for each qualifying child as the additional child tax credit (claimed on Form 8812; shown below) |

| Income threshold at which the CTC phases out is increased to $400,000 for married filing jointly |

| Qualifying children must have a Social Security Number issued by the Social Security Administration before the due date of your return to be eligible for the CTC or ACTC |

|

| Top |

| Credit for Other Dependents |

| New nonrefundable credit of up to $500 for each qualifying dependent (other than children claimed for CTC) |

| Qualifying dependent must be a U.S. citizen, U.S. national, or U.S. resident alien |

| Credit is calculated with the child tax credit in the form instructions |

| Total of both credits are subject to a single phase out when AGI exceeds $200,000 or $400,000 if married filing jointly |

| Top |

| Alternative Minimum Tax (AMT) Exemption |

| The AMT exemption amount is increased to $70,300 ($109,400 MFJ) |

| Income level at which AMT exemption begins to phase out has increased to $500,000 ($1,000,000 MFJ) |

| Top |

| Alimony Payments |

| Alimony and separate maintenance payments are not deductible for any divorce or separation agreement executed after December 31, 2018 |

| Alimony or separate maintenance payments are not included in income for any divorce or separation agreement executed after December 31, 2018 |

| Top |

| Student Loans |

| Student loans that are discharged due to death or disability are not included in income beginning January 1, 2018 |

| Top |

| Combat Zone Tax Benefits |

| Members of the U.S. Army, U.S. Navy, U.S. Marines, U.S. Air Force, and U.S. Coast Guard who performed services in the Sinai Peninsula can claim combat zone tax benefits retroactive to June 2015; see Publication 3, Armed Forces Tax Guide |

| Top |

| Health Care Coverage |

| For 2018, you must continue to report coverage, exemption status, or an individual shared responsibility payment |

| The shared responsibility payment is reduced to zero under TCJA for tax year 2019 and all subsequent years |

|

| Top |

| Retirement Plans |

Recharacterization of a Roth Conversion

|

| Example - Taxpayer A converts his traditional IRA to a Roth IRA in January 2018. All contributions that were previously deductible are included in Taxpayer A's income for 2018. After the conversion, the value of the assets in the Roth IRA decline; under prior rules, Taxpayer A was able to reverse the conversion (and effectively not include the converted balance in income) by recharacterizing the IRA as a traditional IRA. Then Taxpayer A could later convert his traditional IRA to a Roth IRA (reconversion), including only the lower value in income. New law closes this loophole. |

Plan Loans to an Employee that Leaves Employment

|

Disaster Relief

|

| Top |

| ABLE Accounts |

Rollover from a 529 Plan

|

Saver's Credit

|

Changes for Taxpayers with Disabilities

|

| Top |

| 529 Plans Allow for K-12 Education |

| The TCJA allows distributions from 529 plans to be used to pay up to $10,000 of tuition per beneficiary (regardless of the number of contributing plans) each year at an elementary or secondary (K-12) public, private or religious school of the beneficiaries choosing |

| Top |

| Maximum Rates on Capital Gains & Qualified Dividends |

| The provision generally retains the present-law maximum rates on net capital gain and qualified dividends. The breakpoints are based on the same amounts as the breakpoints under present law, except the breakpoints are indexed using the C-CPI-U in taxable years beginning after December 31, 2017. (see table on next slide) |

| Chained Consumer Price Index for All Urban Consumers (C-CPI-U) |

| Unlike the CPI-U, the C-CPI-U accounts for the ability of individuals to alter their consumption patterns in response to relative price changes. The C-CPI-U accomplishes this by allowing for consumer substitution between item categories in the market basket of consumer goods and services that make up the index, while the CPI-U only allows for modest substitution within item categories. |

| The provision requiring C-CPI-U indexing after 2017 is permanent |

| Top |

| New Capital Gain Breakpoints for 2018 | ||

| Filing Status | 15-percent Breakpoint | 20-percent Breakpoint |

| Married Individuals Filing Joint Returns and Surviving Spouses | $77,200 | $479,000 |

| Married Individuals Filing Separate | $38,600 | $239,500 |

| Heads of Household | $51,700 | $452,400 |

| Single Individuals (other than Surviving Spouses and Heads of Households) | $38,600 | $425,800 |

| Estates and Trusts | $2,600 | $12,700 |

| Top | ||

| Filing Status |

| In general, filing status depends on marital status. The IRS considers a person unmarried for the whole year if - on the last day of the tax year - he/she is unmarried or legally separated from a spouse under a divorce or separate maintenance decree. |

| For federal tax purposes, taxpayers of the same sex are considered married if they were lawfully married in a state (or foreign country) whose laws authorize the marriage of two individuals of the same sex, even if the state (or foreign country) in which they now live does not recognize same-sex marriage. |

Head of Household (HOH)

|

| Top |

| Am I Required to File a Tax Return? | ||

| IF your filing status is . . . | AND at the end of 2018 you were* . . . | THEN file a return if your gross income** was at least . . . |

| Single | under 65 65 or older | $12,000 13,600 |

| Married filing jointly*** | under 65 (both spouses) 65 or older (one spouse) 65 or older (both spouses) | $24,000 25,300 26,600 |

| Married filing separately | any age | $5 |

| Head of household | under 65 65 or older | $18,000 19,600 |

| Qualifying widow(er) | under 65 65 or older | $24,000 25,300 |

| Top | ||

| Schedule C Provisions |

| Meals and entertainment expenses associated with the active conduct of the taxpayer's trade or business have been disallowed and/or limited for 2018 |

| Beginning January 1, 2018, there is NO allowable deduction for entertainment expenses |

Meals expense is deductible if:

|

| Top |

| Section 179 Expense Limits |

| In 2018, the maximum deduction under Section 179 increases to $1 million |

| The phaseout threshold amount increases to $2.5 million for qualifying property placed in service during the year |

| Applies to BOTH new and used property |

| Not allowed for property held for the production of income, such as rental property |

| Expanded to include certain tangible personal property used predominantly to furnish lodging or in connection with furnishing lodging |

| Top |

| 100% Bonus Depreciation |

| Extended to December 31, 2023 |

| Top |

| Sec. 199 - Qualified Business Income Deduction |

| Tax Cuts and Jobs Act, Provision 11011 Section 199A - Qualified Business Income Deduction |

| Eligible taxpayers may be entitled to a deduction of up to 20 percent of qualified business income (QBI) |

| Eligible taxpayers may also be entitled to a deduction of up to 20 percent of their combined qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income |

Qualified Business Income (QBI)

|

Specified Service Trade or Business (SSTB)

|

Phase-in of SSTB limitation

|

Limitation based on W2 wages and capital

|

| Top |

| Taxable Income (TI) | |||

| Type of Business(as per IRS definitions) | TI Less Than $315,000 (MFJ) or $157,000 (AOF) | TI Between: $315,000-$415,000 (MFJ) or $157,500-$207,500 (AOF) | TI Greater than: $415,000 (MFJ) or $207,500 (AOF) |

| Specified Service Trade or Business (SSTB) | 199A Deduction allowed with no limits | Must complete Sch A; then 199A Deduct. is reduced by % of income that exceeds TI threshold &/ or W2 wages and qualified property | $0 Deduction |

| Qualified Trade or Business (Non-service) | 199A Deduction allowed with no limits | 199A Deduction is reduced according to the % of income that exceeds the TI threshold amount | 199A Deduction calculated as the lesser of (1) 20% of TI or (2) the greater of (a) 50% of W2 wages or (b) 25% of W2 wages plus 2.5% of qualified property |

| TI - Taxable Income | MFJ - Married filing Jointly | AOF - All Other Filers | |

| Top | |||

| Software Changes |

| Qualified business income is still input as Schedule C, Schedule E, Schedule F or pass-through income from Schedule K-1's |

| Under the 'Deductions and Credits' tab there is a new section labeled 'Qualified Business Income Deduction (Section 199A Deduction)' |

|

| Each QBI activity must be added so the software prepares the calculation for 199A |

|

| When you add the QBI activity, the software will show you the calculation; adjustments can be made on this screen |

|

| Top |

| Section 199A Calculation |

| Depending on the AGI, the software will produce a Simplified Worksheet or a more detailed worksheet |

| Both worksheets will show you the QBI Deduction the taxpayer qualifies for on the tax return |

| No specific form associated with Section 199A; entered on line 9 of Form 1040 |

|

|

| Top |

| Kiddie Tax Modifications |

| TCJA simplifies the "kiddie tax" by applying ordinary and capital gains rates applicable to trusts and estates to the net unearned income of a child |

| Effectively, the child's tax is unaffected by the tax situation of the child's parents or the unearned income of any siblings |

| Top |

Get more for your money with OLT!

PRICE COMPARISON

Copyright @ 2018 - 2025 ON-LINE TAXES. All Rights Reserved